Vehicle Insurance in India

Vehicle insurance in India is a type of general insurance that provides financial protection to vehicle owners against losses or damages arising from accidents, theft, natural disasters, or third-party liabilities. It is mandatory under the Motor Vehicles Act, 1988 for all vehicles operating on Indian roads.

Types of Vehicle Insurance Policies

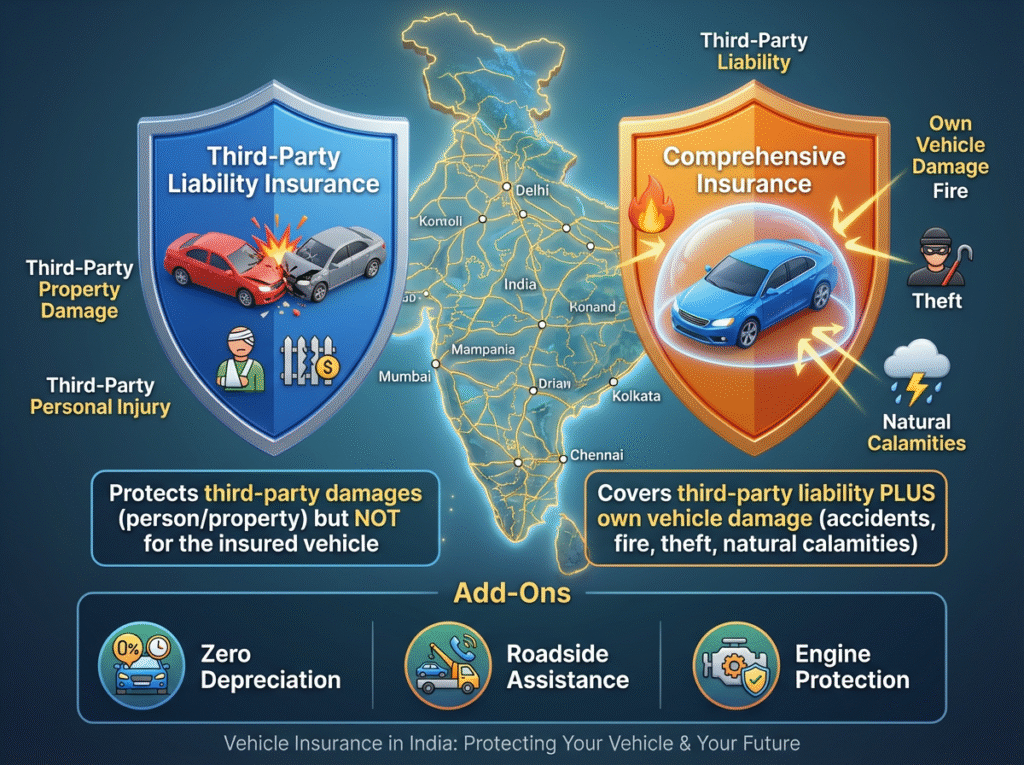

🔹 Third-party coverage

provides legal liability protection for damages to other parties' property (Third Party Property Damage - TPPD) and for injuries or death to individuals (unlimited coverage, as determined by the court). However, it does not cover damage to the insured vehicle itself, which is a requirement by law for all vehicle owners.

🔹 Comprehensive Insurance

• Covers third-party liability plus own damage (accidents, fire, theft, natural calamities). • Optional, but recommended for complete protection.

🔹 Key Inclusions in Comprehensive Plans:

• Accidents • Theft • Fire & explosion • Natural calamities (floods, earthquakes) • Man-made events (riots, strikes) • Personal accident cover for the owner-driver

🔹 Key Exclusions:

• Regular wear and tear • Driving without a valid license or under intoxication • Mechanical/electrical breakdown • Usage outside of geographical limits

🔹 Add-Ons Available (for extra premium):

• Zero depreciation cover • Roadside assistance • Engine protection • Return to invoice • NCB (No Claim Bonus) protection

🔹 Renewal & Claims:

• Policies are typically renewed annually. • Claims can be cashless (at network garages) or reimbursement-based. Would you like help comparing policies or drafting a renewal request?

provides legal liability protection for damages to other parties' property (Third Party Property Damage - TPPD) and for injuries or death to individuals (unlimited coverage, as determined by the court). However, it does not cover damage to the insured vehicle itself, which is a requirement by law for all vehicle owners.

🔹 Comprehensive Insurance

• Covers third-party liability plus own damage (accidents, fire, theft, natural calamities). • Optional, but recommended for complete protection.

🔹 Key Inclusions in Comprehensive Plans:

• Accidents • Theft • Fire & explosion • Natural calamities (floods, earthquakes) • Man-made events (riots, strikes) • Personal accident cover for the owner-driver

🔹 Key Exclusions:

• Regular wear and tear • Driving without a valid license or under intoxication • Mechanical/electrical breakdown • Usage outside of geographical limits

🔹 Add-Ons Available (for extra premium):

• Zero depreciation cover • Roadside assistance • Engine protection • Return to invoice • NCB (No Claim Bonus) protection

🔹 Renewal & Claims:

• Policies are typically renewed annually. • Claims can be cashless (at network garages) or reimbursement-based. Would you like help comparing policies or drafting a renewal request?

Types of Vehicle Insurance Policies

🔹 Third-party coverage

provides legal liability protection for damages to other parties' property (Third Party Property Damage - TPPD) and for injuries or death to individuals (unlimited coverage, as determined by the court). However, it does not cover damage to the insured vehicle itself, which is a requirement by law for all vehicle owners.

🔹 Comprehensive Insurance

• Covers third-party liability plus own damage (accidents, fire, theft, natural calamities). • Optional, but recommended for complete protection.

🔹 Key Inclusions in Comprehensive Plans:

• Accidents • Theft • Fire & explosion • Natural calamities (floods, earthquakes) • Man-made events (riots, strikes) • Personal accident cover for the owner-driver

🔹 Key Exclusions:

• Regular wear and tear • Driving without a valid license or under intoxication • Mechanical/electrical breakdown • Usage outside of geographical limits

🔹 Add-Ons Available (for extra premium):

• Zero depreciation cover • Roadside assistance • Engine protection • Return to invoice • NCB (No Claim Bonus) protection

🔹 Renewal & Claims:

• Policies are typically renewed annually. • Claims can be cashless (at network garages) or reimbursement-based. Would you like help comparing policies or drafting a renewal request?

provides legal liability protection for damages to other parties' property (Third Party Property Damage - TPPD) and for injuries or death to individuals (unlimited coverage, as determined by the court). However, it does not cover damage to the insured vehicle itself, which is a requirement by law for all vehicle owners.

🔹 Comprehensive Insurance

• Covers third-party liability plus own damage (accidents, fire, theft, natural calamities). • Optional, but recommended for complete protection.

🔹 Key Inclusions in Comprehensive Plans:

• Accidents • Theft • Fire & explosion • Natural calamities (floods, earthquakes) • Man-made events (riots, strikes) • Personal accident cover for the owner-driver

🔹 Key Exclusions:

• Regular wear and tear • Driving without a valid license or under intoxication • Mechanical/electrical breakdown • Usage outside of geographical limits

🔹 Add-Ons Available (for extra premium):

• Zero depreciation cover • Roadside assistance • Engine protection • Return to invoice • NCB (No Claim Bonus) protection

🔹 Renewal & Claims:

• Policies are typically renewed annually. • Claims can be cashless (at network garages) or reimbursement-based. Would you like help comparing policies or drafting a renewal request?

Key Definitions as per IRDA

IDV (Insured Declared Value)

Represents the current market value of the vehicle and serves as the basis for claim settlement in case of theft or total loss.

Determines the premium.

Defines the maximum claim amount.

A lower IDV reduces premiums but may lead to lower claim payouts.

NCB (No Claim Bonus)

A discount for not making any claims during the policy term, rewarding safe driving. Applicable only on Own Damage (OD) Premium. Increases with consecutive claim-free years, up to 50%. Transferable when switching insurers. Lapses if a claim is made or policy isn’t renewed within 90 days of expiry.

NCB Discount Slab:1 year: 20%

2 years: 25%

3 years: 35%

4 years: 45%

5+ years: 50%

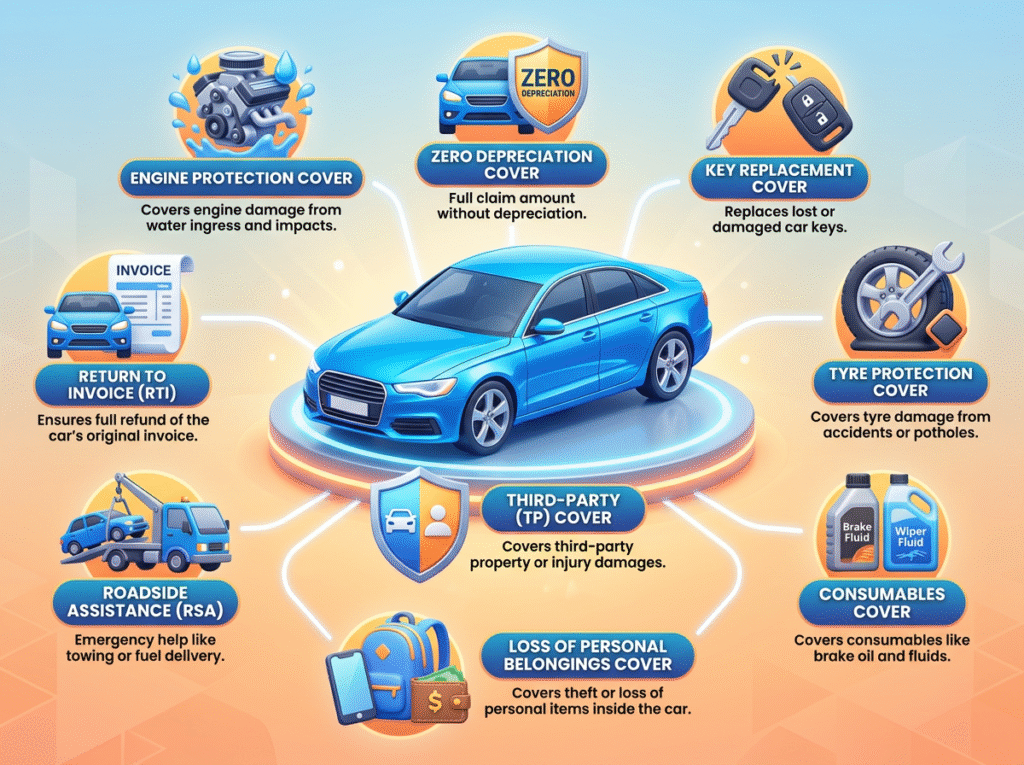

Add-On Covers

Zero Depreciation Cover

Zero Depreciation Cover (also called Nil Depreciation or Bumper-to-Bumper Cover) is an add-on rider available with comprehensive car insurance policies in India. It ensures that no depreciation is deducted on the value of replaced parts during a claim settlement, meaning you receive the full claim amount without any deduction for part wear and tear.

Loss of Personal Belongings Cover

Loss of Personal Belongings Cover is an optional add-on in vehicle insurance in India that provides reimbursement for the loss or theft of personal items kept inside your insured vehicle at the time of an accident, theft, or break-in.

Engine Protection Cover

In India, Engine Protection Cover is an optional add-on to a comprehensive motor insurance policy. It provides financial protection against damages to the engine and its internal components, which are typically not covered under standard comprehensive policies. This cover is especially beneficial in scenarios like water ingress during monsoons, which can lead to engine failure.

Key Features of Engine Protection Cover

• Coverage: Typically includes repair or replacement costs for internal engine parts like pistons, crankshaft, cylinder head, and gearbox components due to damages from water ingress, oil leakage, or accidental undercarriage impacts.

• Exclusions: Generally excludes damages due to regular wear and tear, negligence (e.g., attempting to start a water-logged engine), and pre-existing engine issues.

• Claim Conditions: Some insurers may require that the vehicle be repaired at authorized workshops to avail full claim benefits. For instance, certain policies stipulate that if repairs are done at non-authorized workshops, the insurer’s liability may be limited to a percentage (e.g., 75%) of the assessed claim amount.

• Impact on No Claim Bonus (NCB): Filing a claim under this add-on may affect the NCB of your base policy.

Key Features of Engine Protection Cover

• Coverage: Typically includes repair or replacement costs for internal engine parts like pistons, crankshaft, cylinder head, and gearbox components due to damages from water ingress, oil leakage, or accidental undercarriage impacts.

• Exclusions: Generally excludes damages due to regular wear and tear, negligence (e.g., attempting to start a water-logged engine), and pre-existing engine issues.

• Claim Conditions: Some insurers may require that the vehicle be repaired at authorized workshops to avail full claim benefits. For instance, certain policies stipulate that if repairs are done at non-authorized workshops, the insurer’s liability may be limited to a percentage (e.g., 75%) of the assessed claim amount.

• Impact on No Claim Bonus (NCB): Filing a claim under this add-on may affect the NCB of your base policy.

Return to Invoice (RTI) Cover

Return to Invoice (RTI) Cover is an add-on in comprehensive vehicle insurance in India that helps bridge the gap between the Insured Declared Value (IDV) of your vehicle and the original invoice value, in case of total loss or theft of the vehicle. .

⸻ Key Features of Return to Invoice Cover: .

Coverage: Pays the original invoice value (on-road price) of the car, including road tax and registration fees, instead of just the depreciated IDV. .

When it Applies: Only in case of total loss, constructive total loss, or irrecoverable theft. .

Eligibility:Usually available for vehicles up to 3 years old (varies by insurer) .

Replacement Benefit: Some insurers even offer replacement of a brand new vehicle of same make & model. .

Add-On Premium: Generally a small % of total premium (varies by car value and insurer) .

⸻ Key Features of Return to Invoice Cover: .

Coverage: Pays the original invoice value (on-road price) of the car, including road tax and registration fees, instead of just the depreciated IDV. .

When it Applies: Only in case of total loss, constructive total loss, or irrecoverable theft. .

Eligibility:Usually available for vehicles up to 3 years old (varies by insurer) .

Replacement Benefit: Some insurers even offer replacement of a brand new vehicle of same make & model. .

Add-On Premium: Generally a small % of total premium (varies by car value and insurer) .

Tyre Protection Cover

Tyre Protection Cover is an optional add-on to a comprehensive car insurance policy in India. It provides financial coverage for repair or replacement of tyres and tubes damaged due to accidental means, such as potholes, cuts, bursts, or road debris—which are not typically covered under standard insurance

Roadside Assistance (RSA) Cover

RSA Cover stands for Roadside Assistance Cover, an optional add-on in vehicle insurance in India that provides 24x7 emergency help if your vehicle breaks down or becomes immobilized while on the road.

Key Replacement Cover

Key Replacement Cover is an optional add-on in vehicle insurance that reimburses the cost of replacing lost, stolen, or damaged vehicle keys and locks. It can be added to a comprehensive car insurance policy for an extra premium.

Loss of Personal Belongings Cover

Loss of Personal Belongings Cover is an optional add-on in vehicle insurance in India that provides reimbursement for the loss or theft of personal items kept inside your insured vehicle at the time of an accident, theft, or break-in.

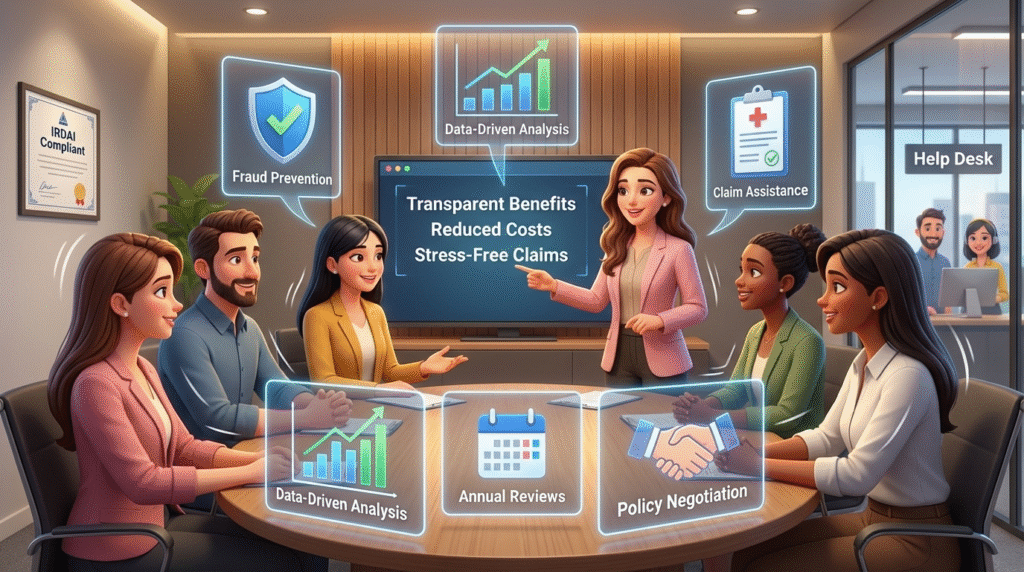

How Insurance Mart Advisors Resolve These Issues – In Depth

At Insurance Mart, we go beyond selling policies—we act as your long-term insurance partner, ensuring both employees and employers get the best value with minimal hassle. Our dedicated claims support team provides personalized assistance, fast processing, and clear communication, guiding employees step-by-step to reduce stress and improve trust in the benefits program. We optimize policies to maximize employee coverage without overlaps, educate staff on effective usage, and promote preventive care to reduce future claims. For employers, we use data-driven analysis, custom plan structuring, and strong negotiation skills to keep costs predictable while maintaining quality coverage. We also ensure full compliance with IRDAI and labor laws, assist in audits, and implement fraud prevention measures to reduce legal and financial risks. With annual reviews, continuous year-round support, and feedback-driven improvements, we create a stable, transparent, and value-driven benefits environment where employees feel supported and employers stay in control of costs.