No Claim Bonus Health Insurance: Meaning, Benefits & How It Works

When we think about health insurance, we often focus on two things: the premium we pay and the sum insured we get. But there is a third, powerful element that often goes unnoticed until several years down the line—the no claim bonus health insurance benefit.

For many policyholders, health insurance is a safety net they hope never to use. But did you know that staying healthy and not making claims can actually make you wealthier in terms of coverage? In an era where medical inflation is rising at double digits in India, your base sum insured might not be enough five years from now. This is where the No Claim Bonus (NCB) steps in as a silent guardian, boosting your financial protection without costing you a single extra rupee.

At Insurance Mart, we believe that buying a policy is just the first step. Understanding how to maximize its benefits—like the NCB—is what truly secures your financial future. In this guide, we will break down exactly how this bonus works, the common mistakes to avoid, and how it can eventually double your coverage amount.

What Is No Claim Bonus in Health Insurance?

To put it simply, what is no claim bonus in health insurance? It is a reward given by insurance companies to policyholders for not filing a claim during a policy year.

Think of it as a “good health reward.” If you go through a full year without hospitalization or reimbursing medical expenses, the insurer acknowledges this low risk.

However, there is a crucial difference between how this works in health insurance versus other types. In motor insurance, for example, the NCB is typically given as a discount on the renewal premium. In health insurance, the standard practice is different. Instead of lowering your premium, insurers usually offer a Cumulative Bonus, which increases your total Sum Insured (coverage amount) for the same premium.

For instance, if you have a policy of ₹5 Lakh and you don’t claim this year, your insurer might increase your cover to ₹5.5 Lakh next year, while your premium remains based on the original ₹5 Lakh structure (subject to age-slab changes).

How No Claim Bonus Works in Health Insurance

Understanding the mechanics of this benefit is essential for long-term planning. Here is a breakdown of how no claim bonus works in health insurance.

Most insurers in India follow a percentage-based structure. The Insurance Regulatory and Development Authority of India (IRDAI) allows insurers to design their own bonus structures, but they generally fall into two categories:

- Standard Cumulative Bonus: The insurer increases your sum insured by a fixed percentage (usually 5% to 10%) for every claim-free year.

- Super Cumulative Bonus: Some modern, premium policies offer a massive jump, increasing the sum insured by 50% or even 100% for every claim-free year.

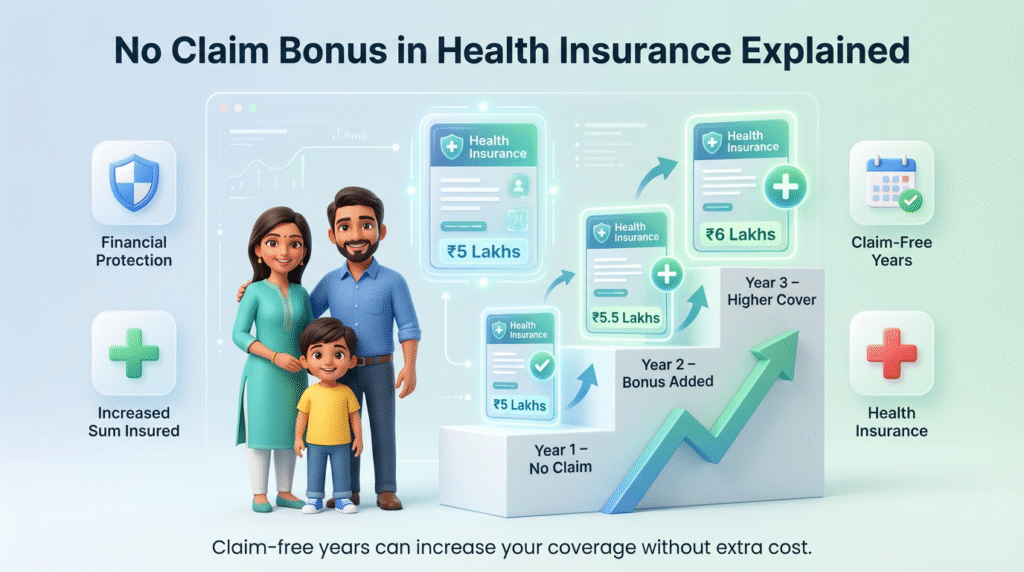

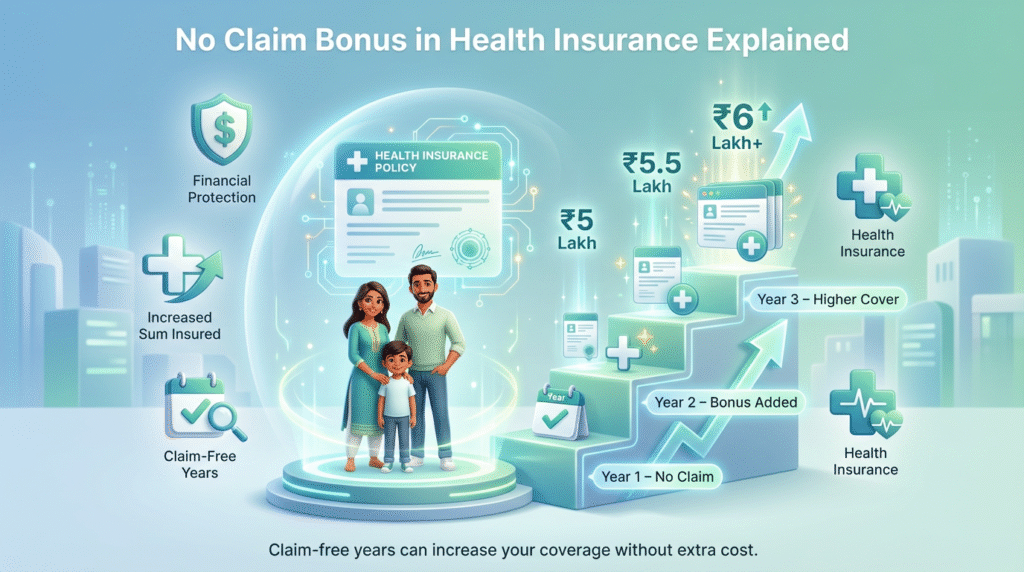

The Mechanics of Growth

Let’s assume you have a health policy with a Sum Insured of ₹10 Lakh. The policy offers a 10% NCB for every claim-free year, up to a maximum of 100%.

- Year 1: You buy a ₹10 Lakh cover. You make no claims.

- Year 2: Upon renewal, your cover becomes ₹11 Lakh (10% increase). You pay the premium for ₹10 Lakh.

- Year 3: Another claim-free year. Your cover becomes ₹12 Lakh.

This continues until you hit the “Cap.” Most policies have a maximum limit on how much the NCB can grow—usually up to 100% or 150% of the base sum insured. Once you hit that cap, your coverage stops increasing, even if you don’t claim.

What Happens If You Claim?

This is the most critical part of how no claim bonus works in health insurance. If you make a claim in a policy year, your accumulated bonus usually reduces at the same rate it accrued. However, your Base Sum Insured will never reduce.

No Claim Bonus Health Insurance Explained with Real-Life Examples

To truly grasp the impact, let’s look at no claim bonus health insurance explained through different scenarios typical for Indian families.

1. The Young Professional (Individual Policy)

Ravi, 28, buys a ₹5 Lakh policy. He is healthy and doesn’t visit the hospital for 5 years. His policy offers a 20% NCB per year.

- Start: ₹5 Lakh cover.

- End of Year 5: His coverage has effectively doubled to ₹10 Lakh.

When Ravi eventually needs hospitalization in his 30s, he has a ₹10 Lakh shield, despite only paying premiums for a ₹5 Lakh policy.

2. The Sharma Family (Family Floater)

The Sharmas have a ₹10 Lakh floater policy covering husband, wife, and two kids. In a floater plan, the NCB applies to the entire policy, not individuals.

- Scenario: For 3 years, they make no claims. Their cover grows to ₹13 Lakh.

- The Event: In the 4th year, the youngest child is hospitalized for dengue.

- The Result: Because a claim was made, the NCB for the entire family will reduce during the next renewal. This highlights why preserving NCB in family plans is harder but highly rewarding.

3. Senior Citizens

For seniors, base premiums are very high. Getting a higher sum insured (e.g., ₹20 Lakh) might be unaffordable initially. By purchasing a lower sum insured early (e.g., at age 60) and maintaining health, a senior citizen can gradually increase their cover via NCB, combating medical inflation without a drastic spike in premiums.

Benefits of No Claim Bonus in Health Insurance

Why should you prioritize a policy with a strong NCB structure? Here are the primary benefits of no claim bonus in health insurance:

1. Higher Coverage at No Extra Cost

This is the most obvious benefit. You essentially get free insurance coverage. In a market where raising your sum insured manually requires paying a significantly higher premium, NCB does it for free.

2. A Hedge Against Medical Inflation

Healthcare costs in India are skyrocketing. A surgery that costs ₹3 Lakh today might cost ₹5 Lakh five years from now. If your sum insured stays static, you are losing value. The NCB ensures your coverage grows alongside inflation, keeping you adequately protected.

3. Buffer for Critical Illnesses

Serious ailments like cancer or cardiac issues often require prolonged treatment that exceeds basic sum insured limits. An accumulated NCB can provide that critical buffer of extra funds, reducing your out-of-pocket expenses.

4. Incentive for Preventive Health

Knowing that your coverage will increase if you stay healthy acts as a financial motivation to maintain a healthy lifestyle and utilize preventive check-ups rather than waiting for an illness to escalate to hospitalization.

How No Claim Bonus Impacts Your Health Insurance Claim

Having a high no claim bonus health insurance balance changes the game when you actually need to use your card at the hospital.

Imagine you have a base policy of ₹5 Lakh, and over the years, you have accumulated ₹5 Lakh in NCB. Your total available pool is ₹10 Lakh.

If you undergo a major surgery costing ₹8 Lakh:

- Without NCB: The insurer pays ₹5 Lakh. You pay ₹3 Lakh from your savings.

- With NCB: The insurer pays the full ₹8 Lakh. Your savings remain untouched.

A Warning on Room Rent Limits

This is an area where expert advice from Insurance Mart is vital. Many policies link their “Room Rent Limit” to the Base Sum Insured, not the accumulated NCB total.

If your base policy is ₹5 Lakh, and your room rent limit is 1% (₹5,000/day), having an NCB that pushes your total cover to ₹10 Lakh might not increase your room eligibility to ₹10,000/day. If you choose a luxury room assuming your total cover allows it, you might face “proportionate deductions” on your entire bill. Always check your policy wording regarding sub-limits.

Common Mistakes That Can Reduce or Cancel Your No Claim Bonus

We often see clients lose their hard-earned bonuses due to simple errors. Here is how to avoid them:

- Making Small, Unnecessary Claims: If you have a hospital bill of ₹8,000 and your NCB is worth ₹1 Lakh of extra cover, claiming that small amount might be unwise. By claiming ₹8,000, you might lose 10% or 20% of your bonus (which could be valued much higher in future protection terms).

- Letting the Policy Lapse: If you do not renew your policy within the grace period, your policy terminates. When you buy a new one, you start from zero. Your accumulated NCB is lost forever.

- Ignoring Portability Benefits: If you are unhappy with your insurer, you can port (switch) to a new one. IRDAI rules allow you to transfer your NCB to the new insurer, but you must declare it correctly during the process.

- Choosing Policies with Weak NCB Terms: Some policies offer only a 5% increase per year, taking 20 years to double. Others offer 50% per year, doubling in just 2 years. Choosing the wrong product slows down your protection growth.

How Insurance Mart Helps You Protect Your No Claim Bonus

At Insurance Mart, we are not just here to sell you a policy; we are here to ensure that policy works for you when you need it most. Our advisory role ensures that your no claim bonus health insurance benefits are optimized.

- Smart Policy Selection: We help you compare policies not just on premium, but on how fast the NCB grows. We analyze the fine print to ensure you get the best “Super Cumulative Bonus” options available.

- Claim Advisory: Before you file a claim for a minor amount, our experts can calculate the long-term impact. We help you decide whether it is financially better to pay a small bill out of pocket to protect a large bonus.

- Renewal Management: We send timely reminders to ensure you never face a policy lapse and the subsequent loss of benefits.

- Portability Assistance: If you want to switch insurers, we handle the paperwork to ensure your accrued credit and NCB are transferred seamlessly.

Whether you are looking for new coverage or need help understanding your current benefits, explore our Medical Insurance services or read more about different Claim Types to stay informed.

FAQs on No Claim Bonus in Health Insurance

1. Does NCB reduce after any claim?

Yes, in most standard policies, making a claim reduces your NCB balance for the next renewal. However, some premium policies offer a feature called “NCB Protect” where the bonus is not reduced for small claims or accidental claims.

2. Is NCB transferable?

Yes. If you decide to port your health insurance policy from Insurer A to Insurer B, your accrued No Claim Bonus is transferable up to the same value, provided the new sum insured matches the old one.

3. Is NCB applicable in group mediclaim?

Generally, no. Corporate or Group Health Insurance policies provided by employers usually do not offer a No Claim Bonus. The cover remains fixed regardless of claim history.

4. Can NCB be restored after a claim?

Once NCB is reduced due to a claim, it can be built back up again in subsequent claim-free years. It is not “restored” instantly but earned back over time.

Conclusion: Use No Claim Bonus as a Long-Term Health Asset

The no claim bonus health insurance benefit is one of the most powerful tools in your financial planning kit. It rewards your good health with free protection, helping you stay ahead of medical inflation.

However, maximizing this benefit requires discipline—timely renewals, prudent claim management, and choosing the right policy structure from day one. Do not let a small oversight wipe out years of accrued benefits.

If you are unsure about your current policy’s bonus structure or need assistance with a renewal to protect your NCB, Contact Insurance Mart today. Let us help you keep your health and your wealth