How Many Times Car Insurance Can Be Claimed? Smart Tips to Protect Your Savings

Many car owners in India share a common worry: “If I make a claim, will my insurer penalize me?” This concern often leads to another important question: how many times can car insurance be claimed in a year? It’s a valid query because the frequency of your claims can significantly impact your policy. It affects everything from your annual premium and your hard-earned No Claim Bonus (NCB) to the insurer’s decision to renew your policy in the future. This guide will provide a clear and complete overview for 2025, helping you understand the rules and consequences of making multiple car insurance claims.

Understanding Car Insurance Claim Limits

The primary purpose of a car insurance policy is to provide financial protection against damages and losses. However, insurance companies are businesses that operate on risk assessment. When a policyholder files frequent claims, it signals a higher risk to the insurer. This can lead to several consequences, such as increased premiums or even non-renewal of the policy. While you pay a premium for coverage, understanding the unwritten rules about claim frequency is crucial for maintaining a healthy and affordable policy in the long run.

Car Insurance Claim Limit Per Year

In India, there is no official rule or law that sets a specific car insurance claim limit per year. Technically, you can file a claim every time your vehicle sustains damage covered by your policy. However, insurance companies monitor claim frequency closely. If you file multiple claims within a single policy year, the insurer might label you as a high-risk customer. This perception can lead them to increase your premium substantially at the time of renewal. In extreme cases, where the claims are frequent and for minor amounts, the insurer might decide not to renew your policy, forcing you to find a new provider who may also charge you a higher premium due to your claims history.

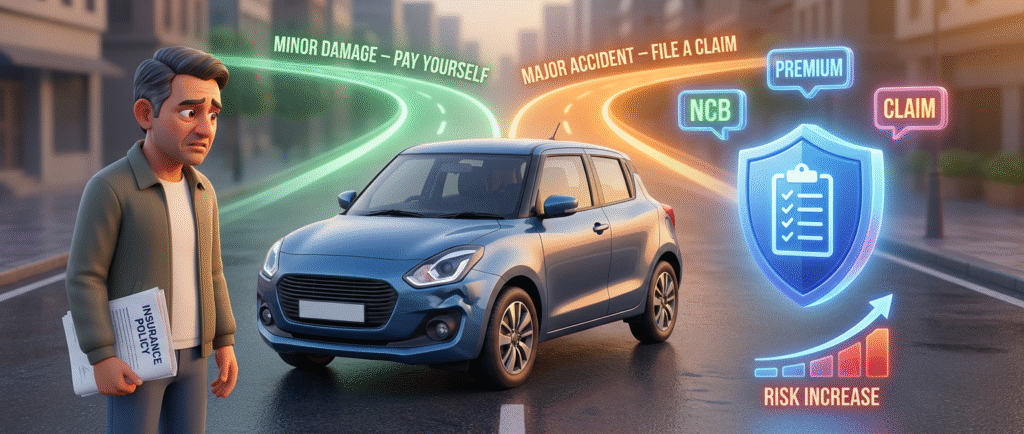

How Many Claims Are Allowed in Car Insurance?

There is no fixed limit on how many times you can make a car insurance claim. You may file multiple claims as long as they are genuine and covered under your policy. However, frequent claims—especially for minor damages—can negatively affect your profile. They usually lead to loss of No Claim Bonus (NCB) and higher premiums at renewal. This is why many experts recommend paying for small repairs yourself to protect your NCB and maintain a good risk profile with your insurer.

Effect of Multiple Car Insurance Claims

Filing multiple claims on your car insurance policy has several direct and indirect consequences. Understanding these effects will help you decide whether filing a claim is the right financial move.

- Premium Increase: This is the most immediate effect. An insurer sees a high-frequency claimant as a liability. To offset the increased risk, they will charge a higher premium when you renew your policy. A history of multiple claims suggests a higher probability of future claims, and the premium is adjusted accordingly.

- Loss of No Claim Bonus (NCB): The NCB is a significant discount on your premium, which can go up to 50% for five consecutive claim-free years. A single claim resets your NCB to zero, resulting in a much higher renewal premium.

- Reduced Insured Declared Value (IDV): The IDV is the maximum amount your insurer will pay in case of total loss or theft. After a major accident and subsequent claim, the insurer might reduce the IDV for the next policy year, as the vehicle’s market value has diminished.

- Higher Deductibles: An insurer might impose a higher voluntary deductible on your policy during renewal. This means you agree to pay a larger portion of the claim amount out of pocket, which lowers the insurer’s liability and can help keep the premium manageable, but increases your upfront cost during a claim.

- Policy Non-Renewal: In rare instances of exceptionally high claim frequency, an insurer might choose not to renew your policy. This can make it difficult to find coverage elsewhere, as other companies will also view your claim history as a red flag.

No Claim Bonus Impact After Multiple Claims

The No Claim Bonus (NCB) is a reward from your insurer for being a safe driver and not making any claims during a policy year. It is one of the most significant factors affecting your renewal premium. The NCB is a discount that accumulates over time, starting at 20% after the first claim-free year and increasing to a maximum of 50% after five consecutive claim-free years.

Here’s how it typically works:

| Claim-Free Years | NCB Discount |

|---|---|

| 1 Year | 20% |

| 2 Consecutive Years | 25% |

| 3 Consecutive Years | 35% |

| 4 Consecutive Years | 45% |

| 5 Consecutive Years | 50% |

The moment you file a claim, this entire accumulated bonus is lost, and your NCB resets to 0% for the next policy year. For example, if you have a 50% NCB and file a claim, your discount for the next renewal will be zero. This can double your premium. To avoid this, some drivers purchase an “NCB Protection” add-on. This add-on allows you to make a specified number of claims (usually one or two) in a policy year without affecting your NCB. It’s a valuable add-on for those who want to safeguard their hard-earned discount.

Car Insurance Claim Rules in India

The Insurance Regulatory and Development Authority of India (IRDAI) has established a set of rules to streamline the claim process and protect policyholders’ interests. Being aware of these rules can make your insurance claim settlement experience much smoother.

Key rules to remember:

- Immediate Intimation: You must inform your insurance company about the incident (accident, theft, etc.) as soon as possible, typically within 24 to 48 hours. Delay in notification can be a reason for claim rejection.

- Surveyor Appointment: Once you report a claim, the insurer is required to appoint a licensed surveyor within 72 hours to assess the damage. The surveyor’s report is a critical document in the claim process.

- Document Submission: You must submit all required documents, such as the claim form, policy copy, registration certificate (RC), driving license, and a First Information Report (FIR) in case of theft, third-party injury, or major accidents.

- FIR is Mandatory For:

- Theft of the vehicle.

- Accidents involving third-party property damage.

- Accidents causing bodily injury or death to a third party.

- Cashless vs. Reimbursement: You can opt for cashless claim assistance at a network garage, where the insurer settles the bill directly with the garage. Alternatively, you can choose reimbursement claim support, where you pay for repairs first and the insurer reimburses you later.

- Total Loss: If the repair cost exceeds 75% of the car’s IDV, the insurer will declare it a total loss and pay you the IDV amount.

Understanding these rules ensures you follow the correct procedure, which is essential for a successful claim. If you need help navigating this process, InsuranceMart Advisors are always available to guide you.

How Many Times Car Insurance Can Be Claimed – Final Verdict

So, how many times can car insurance be claimed? While there is no legal limit, the practical answer is that you should only claim when the repair costs are substantial. For minor damages, it is often wiser to pay out-of-pocket to protect your No Claim Bonus and avoid premium hikes. Every claim you make is recorded and influences how insurers perceive you as a customer. A history of frequent claims will inevitably lead to higher long-term costs. It is essential to weigh the claim amount against the potential loss of your NCB and future premium increases before making a decision. This strategic approach to claims is as important as having other financial protections like bike insurance or health insurance.

Ready to find a car insurance policy that fits your needs and budget? Explore your options on the InsuranceMart Car Insurance page and let our experts help you make an informed choice.

FAQs

1. Is there a limit to how many car insurance claims I can make in a year in India?

No, there is no official limit. However, making multiple claims in a single policy year can lead to higher premiums at renewal and may cause the insurer to consider you a high-risk client.

2. Will my car insurance premium increase after a single claim?

Yes, it is very likely. After a claim, you will lose your No Claim Bonus (NCB), which is a significant discount on your premium. The loss of NCB will result in a higher premium at the time of renewal.

3. When should I avoid filing a car insurance claim?

You should avoid filing a claim for minor damages where the repair cost is less than or slightly more than your NCB discount and applicable deductibles. Paying for small repairs yourself can save you more money in the long run by preserving your NCB.

4. What is an NCB Protection add-on?

NCB Protection is an add-on cover that allows you to make a certain number of claims (usually one or two) within a policy year without your No Claim Bonus being reset to zero. It helps you retain your discount even after making a claim.

5. Can an insurance company refuse to renew my policy if I make too many claims?

Yes, an insurer has the right to refuse renewal of your policy. If you have a history of making frequent claims, the company may see you as an unprofitable customer and decide not to continue the coverage.