Health insurance is supposed to protect you during life’s toughest moments. Unfortunately, many policyholders in India discover that their claims are rejected right when they need financial support the most. Claim Rejections in India

The Insurance Regulatory and Development Authority of India (IRDAI) reports that a large number of health insurance Claim Rejections in India happen because of avoidable mistakes—either by the policyholder or due to lack of awareness.

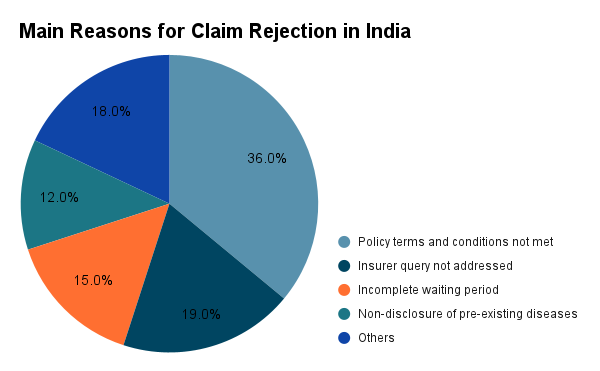

In this blog, we’ll explore the top 10 reasons for claim rejections in India and share practical tips on how you can avoid them.

1. Non-Disclosure of Pre-Existing Diseases

Why Claims Get Rejected:

If you fail to declare medical conditions like diabetes, hypertension, or asthma while buying your policy, insurers may reject claims later.

How to Avoid:

Always disclose your complete medical history honestly. Even if it increases your premium slightly, it ensures full protection during emergencies.

2. Claiming During the Waiting Period

Why Claims Get Rejected:

Most policies have a 30-day initial waiting period (except for accidents) and a 2–4 year waiting period for pre-existing conditions. Filing a claim within this period usually leads to rejection.

How to Avoid:

Understand your policy’s waiting period before relying on it. If you need immediate cover, opt for plans with shorter waiting periods.

3. Incomplete or Incorrect Documentation

Why Claims Get Rejected:

Missing discharge summaries, prescriptions, bills, or submitting handwritten/incomplete documents can lead to delays or outright rejection.

How to Avoid:

Keep every hospital bill, prescription, and medical report. At Insurance Mart, we guide clients step by step to ensure complete documentation for smooth settlement.

4. Claiming Excluded Treatments

Why Claims Get Rejected:

Certain treatments such as dental, cosmetic surgery, infertility treatments, or experimental therapies may be excluded from your policy.

How to Avoid:

Check the exclusion list in your policy documents. If needed, add riders or choose a comprehensive plan that covers your specific needs.

5. Not Informing the Insurer on Time

Why Claims Get Rejected:

Insurers require you to notify them within 24 hours of emergency hospitalization or 48–72 hours for planned treatments.

How to Avoid:

Always inform your insurer or Insurance Mart immediately when hospitalization occurs. Timely intimation is crucial for cashless claims.

6. Choosing Non-Network Hospitals

Why Claims Get Rejected:

If you get treated at a hospital that isn’t part of your insurer’s network hospitals, your cashless claim request can be denied.

How to Avoid:

Before admission, confirm that the hospital is in the network. Keep a list of cashless hospitals handy for emergencies.

7. Violating Room Rent Limits

Why Claims Get Rejected:

If your policy allows ₹5,000/day for room rent but you choose a ₹10,000/day room, the insurer may proportionately reduce the entire bill.

How to Avoid:

Choose a policy with a “No Room Rent Limit” add-on or stay within your entitlement to avoid deductions.

8. Policy Lapse or Non-Renewal

Why Claims Get Rejected:

A lapsed policy is as good as no insurance. If you forget to renew on time, claims during the lapse period are not honored.

How to Avoid:

Set renewal reminders or let Insurance Mart manage your policy renewals so your cover never lapses.

9. Claiming Non-Medical Expenses

Why Claims Get Rejected:

Items like gloves, syringes, masks, PPE kits, or bandages are often excluded from standard plans.

How to Avoid:

Opt for a Consumables Cover add-on to ensure these small but significant costs are covered.

10. Confusion Between OPD and Day Care Coverage

Why Claims Get Rejected:

OPD visits (doctor consultations without admission) are not usually covered, while day care treatments (like dialysis, chemo, cataract surgery) are. Many policyholders confuse the two.

How to Avoid:

Understand your policy coverage clearly. At Insurance Mart, we help you choose policies that suit your healthcare usage.

✅ How to Ensure Your Claim is Approved

- Read Your Policy Carefully: Go beyond premiums—check waiting periods, exclusions, sub-limits, and claim procedures.

- Disclose Everything Honestly: Never hide pre-existing conditions.

- Choose the Right Add-Ons: Riders like consumables cover, no room rent cap, and restoration benefits provide wider protection.

- Keep All Documents Ready: Missing papers are the top cause of claim delays.

- Take Expert Help: Insurance Mart acts as your claim guardian, fighting for full and fair settlements.

Final Thoughts

Health insurance claim rejection can turn a medical emergency into a financial crisis. But with the right knowledge, timely action, and expert guidance, you can avoid these pitfalls.

At Insurance Mart, we don’t just help you buy policies—we stand with you during claims to ensure you get the settlement you deserve.

👉 Facing claim trouble? Click here and let us help you